Real Estate Weekly Outlook: Beyond The Pandemic

Table of Contents

ablokhin/iStock via Getty Images

Real Estate Weekly Outlook

U.S. equity markets finished higher for a second-straight week as relatively solid employment data and strong corporate earnings results – with some exceptions – eased jitters over rising rates and slowing economic growth. Volatility levels remained elevated on another wild week that saw Amazon (AMZN) record the largest single-day increase in market value and Meta Platforms (FB) record the largest single-day decline in market value, underscoring the continued unease as major economies across the globe appear to finally be emerging from the two-year-long pandemic.

Hoya Capital

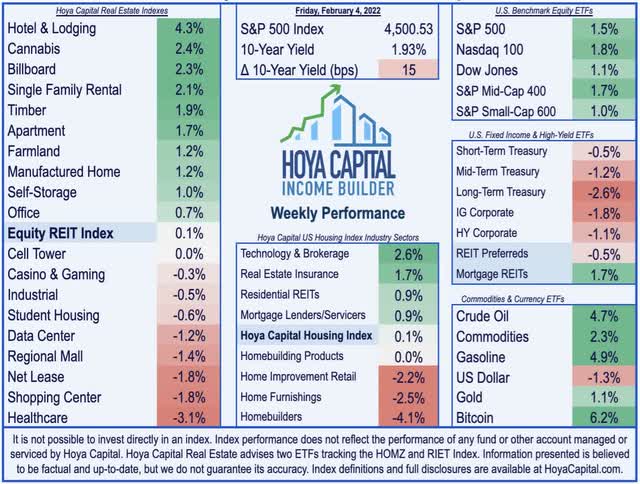

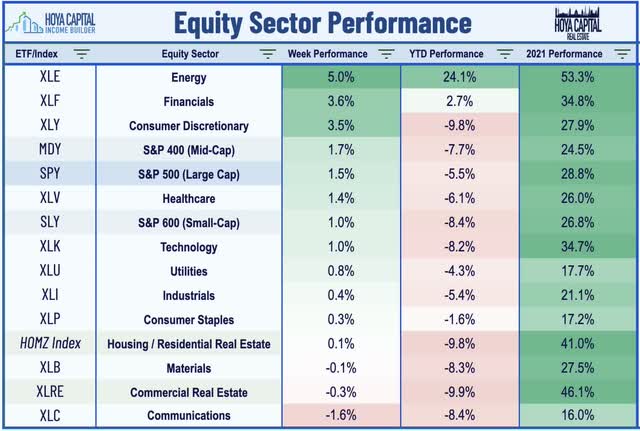

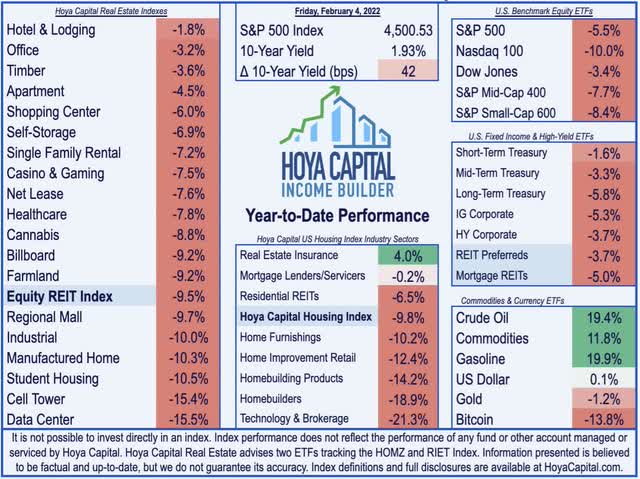

Gaining ground in four-of-five trading sessions after briefly dipping into “correction territory” last week, the S&P 500 (SPY) finished higher by 1.5% on the week and is back within 6% of all-time highs. The tech-heavy Nasdaq 100 (QQQ) gained 1.8% but remains 11% off the highs while the Mid-Cap 400 and Small-Cap 600 are still 10% and 12% below their highs, respectively, despite gains this week. Real estate equities were mixed as stellar earnings reports from residential REITs were offset by weakness from healthcare, retail, and technology REITs. The Equity REIT Index finished higher by 0.1% while Mortgage REITs advanced 1.7%.

Hoya Capital

The solid start to February follows a turbulent January in which the S&P 500 posted monthly declines of 5.3%, its largest since March 2020, while the tech-heavy Nasdaq dipped 9%. The 10-Year Treasury Yield jumped 15 basis points this week to close above 1.90% for the first time since late 2019 after a stronger-than-expected employment report and a solid start to corporate earnings season as 76% of S&P 500 companies have reported EPS above estimates, which likely kept the Federal Reserve on track to begin a potentially aggressive monetary tightening cycle in their upcoming March meeting.

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

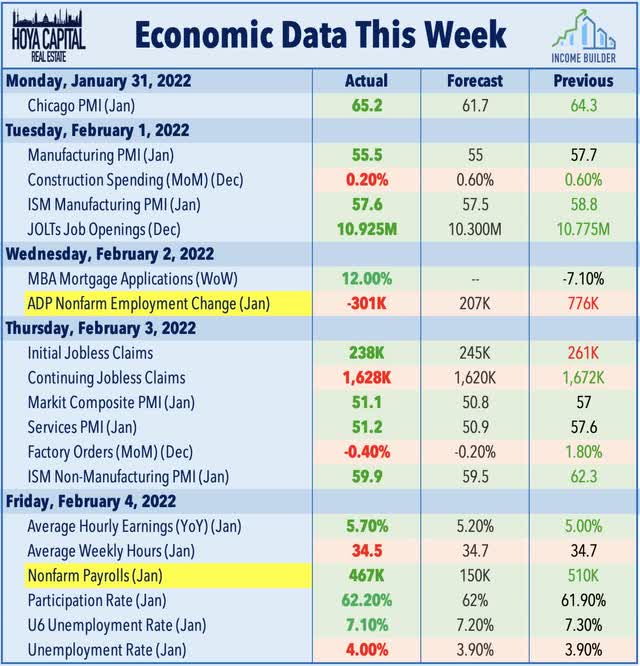

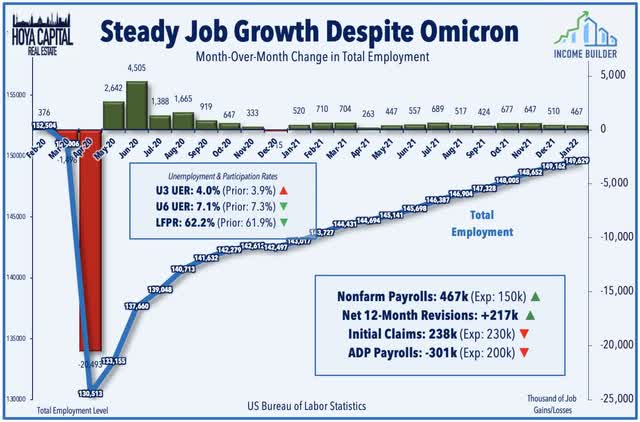

The Bureau of Labor Statistics reported this week that the U.S. economy added 467k jobs in January – well above expectations of roughly 200k – but massive revisions to the past twelve months of data called into question the reliability of the report. The BLS’ annual adjustments resulted in a net gain of 217k jobs above its prior reports, which included upward adjustments of +709k to the past two months, but downward adjustments of -807k to June and July. The upward surprise followed a significantly weaker-than-expected ADP Payrolls report data earlier in the week which showed job losses of 301k in January and an uptick in weekly Jobless Claims throughout January.

Hoya Capital

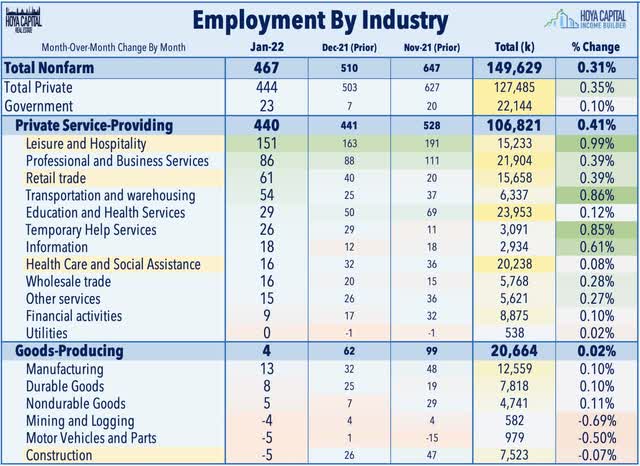

Perplexingly, the report showed that employment continued to trend up in leisure and hospitality and retail trade – two of the most COVID-sensitive categories – despite a concurrence of other data including hotel occupancy, restaurant bookings, and TSA travel data showing a relatively weak January. Interestingly, while it appears that the methodology changes resulted in a brighter picture for the services-side of the economy, the goods-producing sectors saw clear signs of slowing in January, adding just 4k net jobs as hiring in the mining and logging, construction, and motor vehicles sectors were negative in January despite ongoing shortages across the sectors.

Hoya Capital

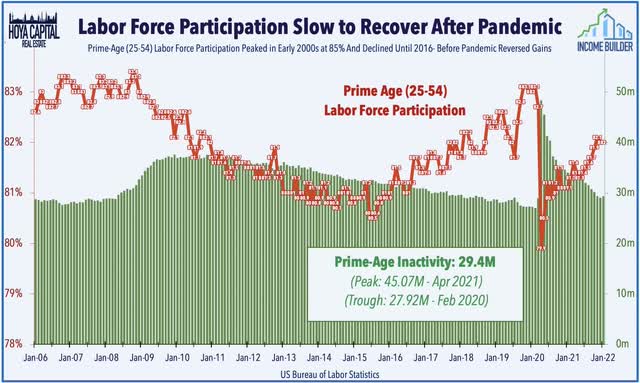

The labor force participation rate – which was also revised higher by the BLS – remains stubbornly depressed and was unchanged at 62.1% in January, which is 1.2 percentage points lower than the pre-pandemic level in February 2020. The employment-population ratio also held steady at 59.7%, which is 1.5 points below its pre-pandemic level. A critical question to determine the path of inflation and interest rates relates to how much “slack” remains in the labor market and what it will take to pull the millions of workers that departed the labor force during the pandemic back into the fold to fill one of the 10.92 million job openings reported this week in the JOLTS report.

Hoya Capital

Equity REIT Week In Review

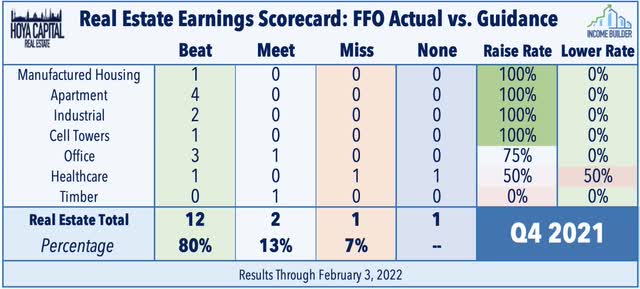

As discussed in our REIT Earnings & Ratings Updates, we’re now two weeks into another newsworthy real estate earnings season with roughly one-third of the real estate sector by market cap reporting fourth-quarter results. Residential REITs have been the upside standouts of earnings season thus far as rents continue to soar by double-digit rates across essentially all markets and segments of the rental markets. REIT earnings have been better than expected thus far with 80% of REITs reporting full-year funds from operations (“FFO”) results that were above the midpoint of their prior guidance.

Hoya Capital

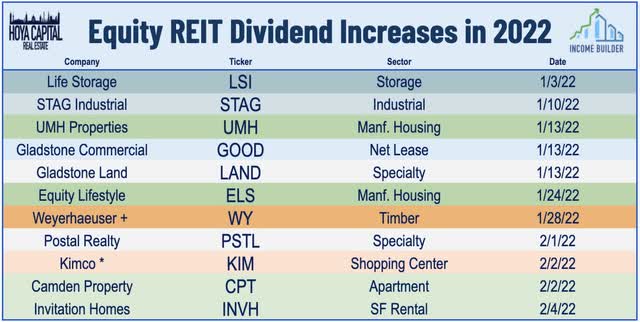

Eleven REITs and a pair of homebuilders have now hiked their dividends thus far in 2022 including four more this past week. Apartment REIT Camden Property (CPT) hiked its dividend by 13%, single-family rental REIT Invitation Homes (INVH) boosted its dividend by 29%, shopping center REIT Kimco’s (KIM) announced an 11.8% dividend hike, and net lease REIT Postal Realty (PSTL) hiked its payout by 1%. We continue to expect a similarly powerful wave of dividend hikes this year as we saw in 2021 when 130 REITs raised their payouts.

Hoya Capital

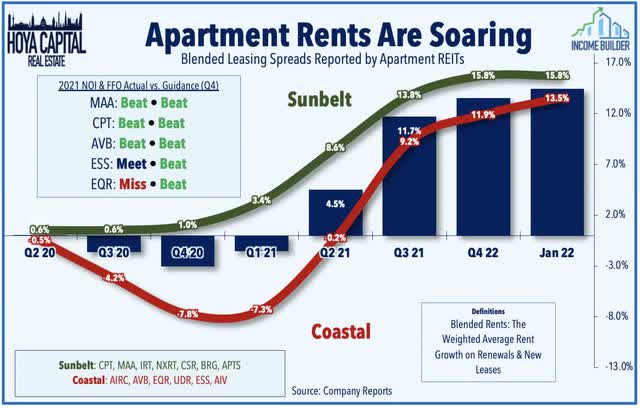

Apartments: Five apartment REITs have reported results this past week and fundamentals across the sector have been stellar with all five REITs reporting double-digit rent growth in late 2021 with a continued acceleration into early 2022. Sunbelt-focused Camden Properties (CPT) rallied 5% on the week and Mid-America Apartments (MAA) gained nearly 4% after these REITs reported blended rent growth of 16% in Q4 and in January – a record-high for both companies. The three Coastal-focused REITs – Equity Residential (EQR), AvalonBay (AVB), and Essex (ESS) – reported rent growth averaging 12% in Q4 and accelerating to 13.5% in January.

Hoya Capital

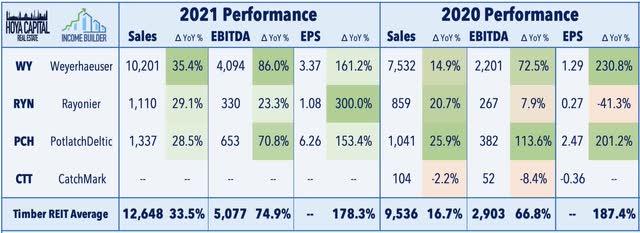

Timber: PotlatchDeltic (PCH) was flat on the week after reporting mixed results as the slump in lumber prices and supply chain constraints resulted in a softer Q4 amid an otherwise record-year across all metrics. PCH delivered full-year revenue growth of nearly 30%, powering a 71% rise in Adjusted EBITDA and a 153% surge in Earnings Per Share. The company provided solid Q1 guidance and commented that “2022 is off to a great start with the recent surge in lumber prices benefitting both our Timberlands and Wood Products businesses. We expect housing-related fundamentals that drive demand in our business to remain favorable.” Rayonier (RYN) gained 3% after reporting solid results with its adjusted EBITDA topping its prior guidance and expects its EBITDA to remain at record levels in 2022 in its initial outlook.

Hoya Capital

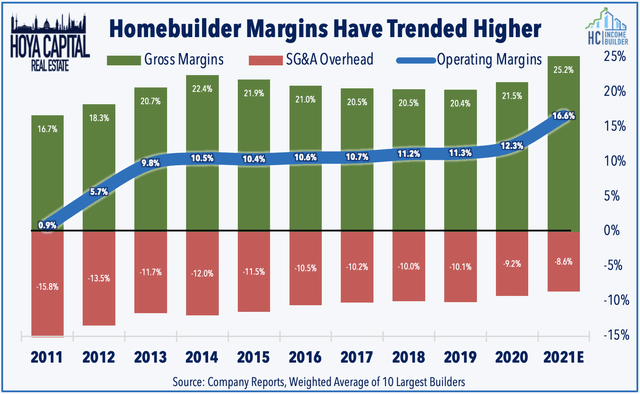

Homebuilders: Sticking in the housing sector, the jump in interest rates pressured homebuilders this past week and pulled the sector back into “bear market” territory – a decline of 20% from their recent highs – despite a very strong slate of earnings reports and strong guidance for 2022 calling for double-digit EPS and revenue growth. DR Horton (DHI) declined 2% despite reporting 37% revenue growth in 2021 and boosting its full-year outlook which calls for growth of another 26%. Margins have been particularly impressive – particularly in results this week from NVR (NVR) and PulteGroup (PHM) – as builders have more-than-offset increased costs through higher sales values. Despite the tough comparable, builders reported a nearly 4 percentage-point increase in operating margins to the highest overall average on record.

Hoya Capital

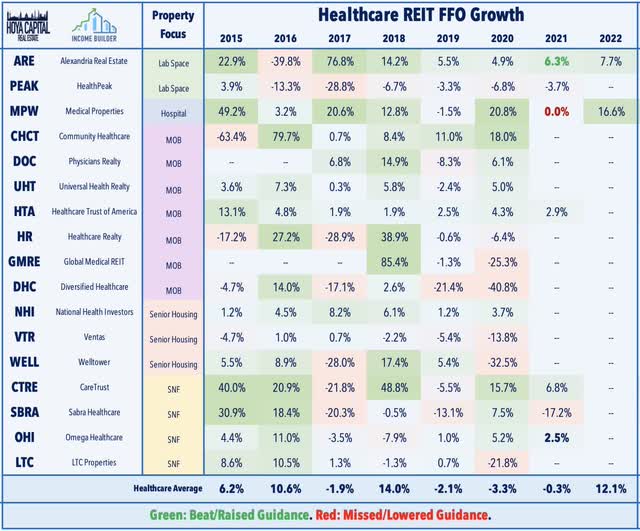

Healthcare: Lab space “sharpshooter” Alexandria Real Estate (ARE) gained 1% on the week after reporting another very strong quarter as lab space continues to be one of the hottest segments of the U.S. real estate market, driving a 25% surge in leasing spreads and 7% NOI growth. However, results from skilled nursing REIT Omega Healthcare (OHI) – which dipped more than 10% – and hospital REIT Medical Properties (MPW) – which declined 2% – reflected Omicron-driven headwinds across the more COVID-sensitive segments of the healthcare sector. For OHI, operator issues remain a headwind with another tenant – representing 3.5% of revenues – not paying its rent, bringing the total up to about 15%. Elsewhere, Diversified Healthcare (DHC) rallied 7% after entering into a $703M joint-venture for 10 medical office properties with two institutional investors.

Hoya Capital

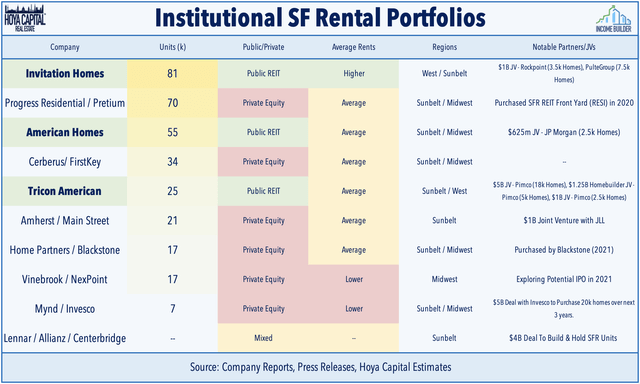

Single-Family Rental: Invitation Homes (INVH) gained 2% on the week after announcing a $250M lead investment to launch Pathway Homes, a new lease-to-own real estate company. Pathway Homes plans to spend an initial $750M acquiring houses on behalf of its customers, who will rent the properties with the option to purchase them. The rent-to-own model has been used by other SFR operators including privately-owned Home Partners of America, which was acquired by Blackstone for $6 billion last year. In our recent report – Meet Your New Landlord – we discussed why the growth trajectory remains promising as the “institutionalization” of the single-family housing market remains in the early innings.

Hoya Capital

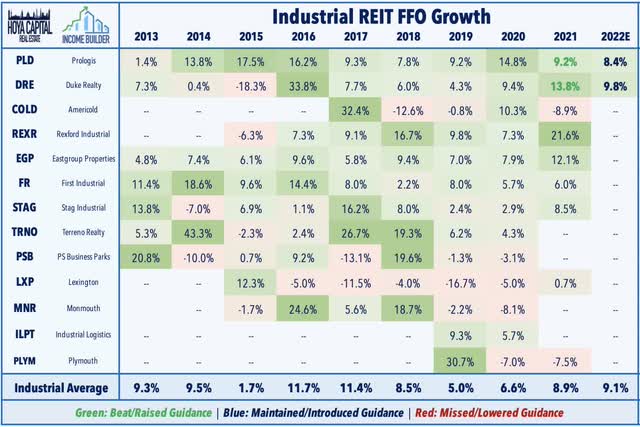

Industrial: LXP Industrial Trust (LXP) gained nearly 5% on the week after it received a $16/share cash offer from activist investor Land & Buildings, which represented a rather modest 11% premium to LXP’s prior closing price of $14.41. LXP announced that its Board will review the letter to determine the course of action that it believes is in the best interests of LXP’s shareholders. As discussed in LXP Industrial: New Name, Uncertain Future, Lexington has delivered disappointing performance over the last decade despite booming demand for industrial real estate. Reports thus far from Prologis (PLD) and Duke Realty (DRE) showed that fundamentals remain stellar across the sector as insatiable demand clashes with limited supply.

Hoya Capital

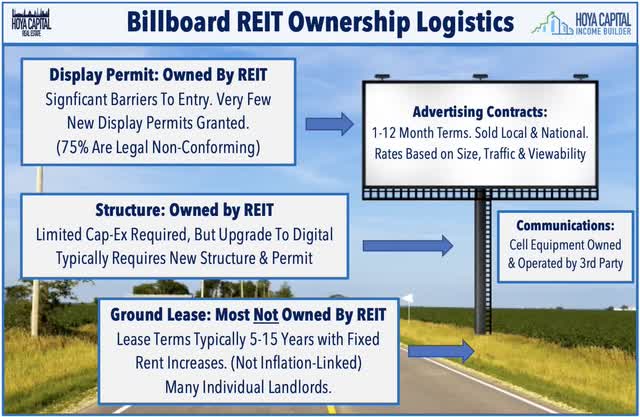

Billboard: This week, we published Billboard REITs: Under-The-Radar Inflation Hedge. We discussed how billboard REITs own a commanding share of the nation’s 500,000 outdoor advertising displays – a surprisingly resilient business with strong inflation-hedging attributes. Unlike other increasingly-cluttered digital formats, there’s “only one channel” on the highway. These REITs are well-positioned to capture the steadily rising share of marketing spending towards Out-of-Home (“OOH”) advertising displays.

Hoya Capital

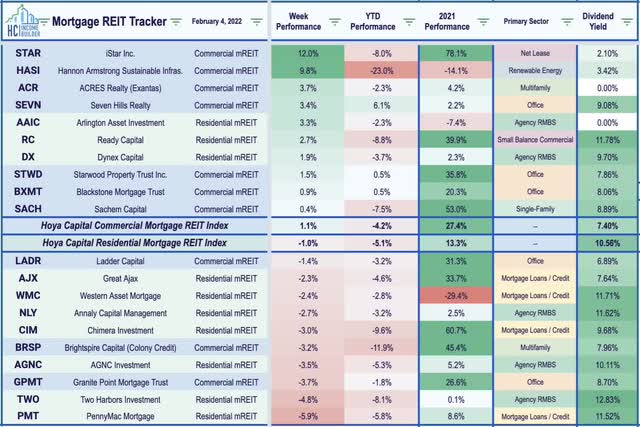

Mortgage REIT Week in Review

Mortgage REITs were mixed on the week as earnings season kicked-off with a trio of reports as commercial mREITs gained 1.1% while residential mREITs declined 1.0%. iStar (STAR) surged 12% on the week after it agreed to sell a portfolio of net lease assets for $3.07B to Carlyle Group which iStar estimates the transaction will net $1.1B of cash proceeds. Dynex Capital (DX) gained nearly 2% after reporting that its BVPS at the end of Q4 was $17.99 – above analyst forecasts – and noted that its BVPS was unchanged in January. DX commented that the Fed “stepping back” from the market represents the “cusp of a significant investment opportunity.”

Hoya Capital

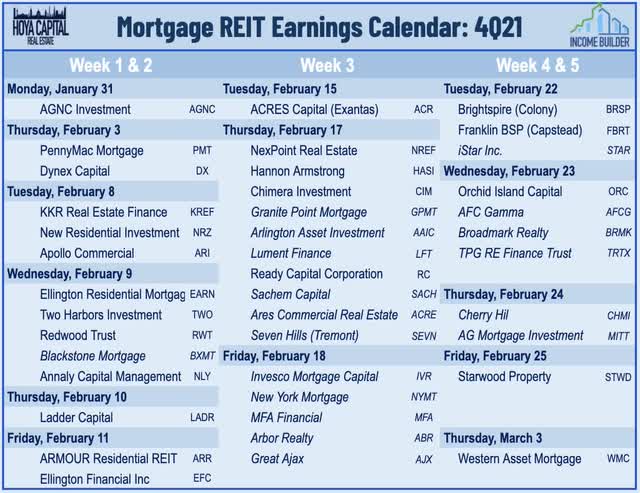

On the downside this past week, AGNC Mortgage (AGNC) finished lower by 3.5% on the week after kicking off mREIT earnings season with a mixed report, noting that its tangible Book Value Per Share (“BVPS”) slipped 4% in Q4 “as spreads to benchmark rates widened moderately and valuations declined relative to interest rate hedges.” However, AGNC noted that while spread widening hurts BVPS in the short term, it improves the expected return on new investments. PennyMac Mortgage (PMT) declined 5.9% on the week after reporting that its BVPS also declined roughly 4% in Q4. We’ll hear reports from ten mREITs next week including New Residential (NRZ), Annaly Capital (NLY), Ladder Capital (LADR), and Two Harbors (TWO).

Hoya Capital

2022 Performance Check-Up & 2021 Review

Through five weeks of 2022, Equity REITs are now lower by 9.5% this year on a price return basis while Mortgage REITs have slipped 5.0%. This compares with the 5.5% decline on the S&P 500 and the 7.7% decline on the S&P Mid-Cap 400. Dragged on the downside by the cell tower and data center sectors, all nineteen REIT sectors are now in negative territory for the year. At 1.93%, the 10-year Treasury yield has climbed 42 basis points since the start of the year and is 141 basis points above its all-time closing low of 0.52% in August 2020, but still 132 basis points below its 2018 peak of 3.25%.

Hoya Capital

Economic Calendar In The Week Ahead

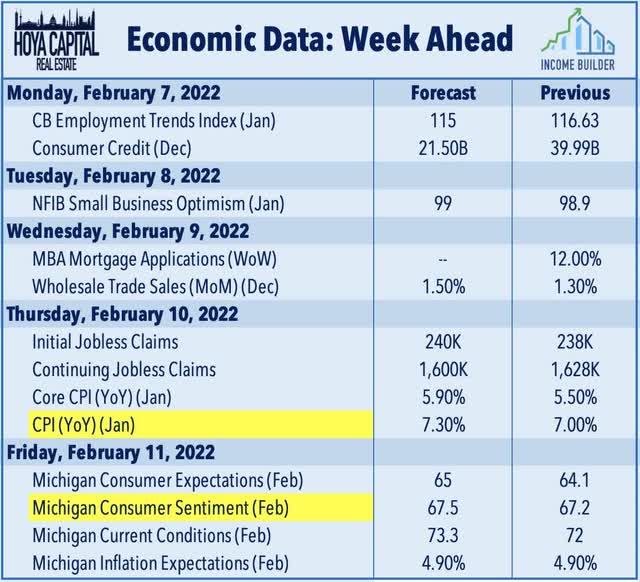

While the earnings calendar remains busy with 82 S&P 500 companies reporting results, the economic calendar slows down a bit in the week ahead with the major report of the week coming on Thursday when the BLS will report the Consumer Price Index for January which is expected to show the highest rate of inflation since 1982. We’ll also be watching Michigan Consumer Sentiment data on Friday which sunk to the lowest level in ten years in January amid lingering concerns over inflation.

Hoya Capital

Last week, we published REIT Earnings Preview: Dividend Hikes And 2022 Outlook. Highlights of next week’s earnings slate include mall REITs Simon Properties (SPG) and Macerich (MAC), net lease REITs W.P. Carey (WPC) and National Realty (NNN), and shopping center REITs Regency Centers (REG), Kimco (KIM), and Federal Realty (FRT). We’ll continue to provide real-time coverage with our Earnings QuickTake posts for Hoya Capital Income Builder members and will publish follow-up articles summarizing our thoughts and analysis throughout earnings season.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Storage, Timber, Prisons, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital